INTRODUCTION:

Restructuring is an important mechanism and, often, an optimum solution for business overhaul as it strengthens a company’s market position, increases its profitability, and streamlines its operations. As economies emerge from the worst of the pandemic, companies across the globe are aggressively considering realigning their organizational structures to improve business efficiencies.

MEANING:

The term merger has not been defined under the Companies Act, 2013 (“CA, 2013”) but in commercial terms, a merger is a combination of two or more existing companies which merge their identities to form a different entity which can either be one of the existing companies or may not be the existing company but may form a separate new entity altogether.

Section 233 of the Companies Act, 2013 introduces the globally accepted concept of Fast Track Merger Process which introduces a slightly simpler procedure for mergers and amalgamations of certain classes of companies including small companies, holding and subsidiary companies. Under this process, it enables these companies to undergo merger and amalgamation procedures quickly, simply and within fixed time duration. The Companies Act, 2013 clearly notifies that it applies to all kinds of compromise and arrangements that involve these companies.

CONDITIONS/ REQUIREMENTS TO BE FULFILLED:

The draft scheme requires approval of

- Board of Directors of both(all) companies.

- 90% of shareholders (in number) and 90% of creditors (in value).

- Central Government (power delegated to Regional Director)

- The scheme must be filed with the Jurisdictional Registrar of Companies (ROC) as well as the official liquidator.

- Convening a meeting of members and creditors to obtain approval. The creditors meeting can be avoided if they readily provide their consent in writing.

- The filing of a declaration of solvency by both the involving companies.

- There is no requirement to submit an auditor’s certificate.

- Now, there is no need to file the scheme before the National Company Law Tribunal (NCLT).

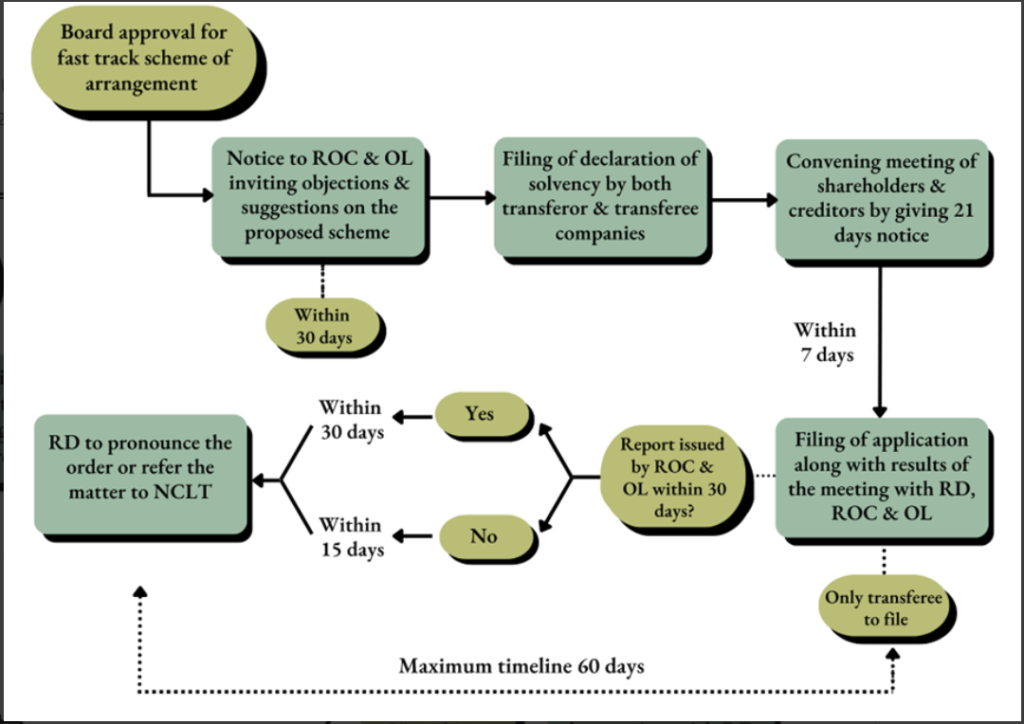

| PROCESS OF FAST TRACK MERGER |

| Discussion & finalization of scheme of arrangement, valuation and other documents |

| Approval of scheme by the BOD of all the companies involved |

| Notice of the proposed scheme to be sent to the ROC, official liquidator and persons affected by the scheme |

| Filing declaration of solvency statement |

| Convening meeting of members & creditors, if any |

| Approval of scheme |

| Filing of report of result of the meeting |

| Confirmation of the scheme |

| Filing order with Registrar of Companies |

| Post Merger compliances |

TIMELINE OF FAST TRACK MERGER:

EFFECTS OF REGISTRATION OF THE SCHEME:

The registration of the scheme has the following effects:

- Property or liabilities are transferred to the transferee company and become properties and liabilities of the transferee company.

- The charges (if any) on the property of the transferor company are applicable and enforceable as the charges on the property of the transferee company.

- Legal proceedings by or against the transferor company are continued by or against the transferee company.

- Where the scheme provides for purchase of shares of the dissenting shareholders or settlement of debt due to dissenting creditors, such amount, to the extent unpaid, becomes the liability of the transferee company.

POST-MERGER EFFECTS & COMPLIANCES:

The registration of the scheme shall have the following effects, namely:

- Transfer of property or liabilities of the transferor company to the transferee company;

- The charges, if any, on the property of the transferor company shall be applicable and enforceable as if the charges were on the property of the transferee company;

- Legal proceedings by or against the transferor company pending before any court of law shall be continued by or against the transferee company;

- Surrender of PAN, IEC, GST, ESI, and PF of the transferor company to the concerned Authorities.

Conclusion

The introduction of fast track mergers under Section 233 of the Companies Act, 2013 is a commendable step towards easing the merger and amalgamation processes for specific classes of companies, particularly small businesses and startups. By eliminating the need for NCLT intervention in most cases, this streamlined mechanism saves companies valuable time and funds. However, ambiguities still exist, such as the scope for step-down subsidiaries and the broader inclusion of associate or Section 8 companies. Additionally, concerns remain about regulatory adherence to statutory timelines and varying interpretations by regional authorities. Despite these challenges, the fast track merger route stands as a significant innovation in India’s corporate restructuring framework—one that promises a more efficient and cost-effective path to mergers and acquisitions.

While Section 233 explicitly mentions holding and subsidiary companies, it does not clearly define the applicability to step-down subsidiaries. In practice, interpretations can vary. Companies are advised to seek professional guidance to confirm eligibility.

Though the Act prescribes a streamlined timeline, delays can occur if regulatory bodies (such as Regional Directors) do not adhere to statutory deadlines. In many cases, the process can be completed significantly faster than the traditional NCLT route, but practical factors may extend the duration.

Post-merger, the transferee company must:

Update records and licenses, including ROC filings.

Surrender the PAN, IEC, GST, ESI, and PF registrations of the transferor company.

Ensure all contractual obligations and legal proceedings are appropriately transitioned.