Notification Ref.

G.S.R. 415(E)

Background & Context

Under the Companies Act, 2013, every qualifying company must spend at least 2% of its average net profits over the preceding three financial years on Corporate Social Responsibility (CSR) activities. The regulatory framework governing deployment of these funds — the Companies (Corporate Social Responsibility Policy) Rules, 2014 — has now received a significant update.

The Ministry of Corporate Affairs (MCA), exercising powers under Section 135 and sub-sections (1) and (2) of Section 469 of the Companies Act, 2013, issued a gazette notification dated 27th May 2026 (G.S.R. 415(E)) to formally amend these Rules, paving the way for CSR expenditure through a new financial instrument issued by Not for Profit Organisations (NPOs) listed on Social Stock Exchanges (SSEs).

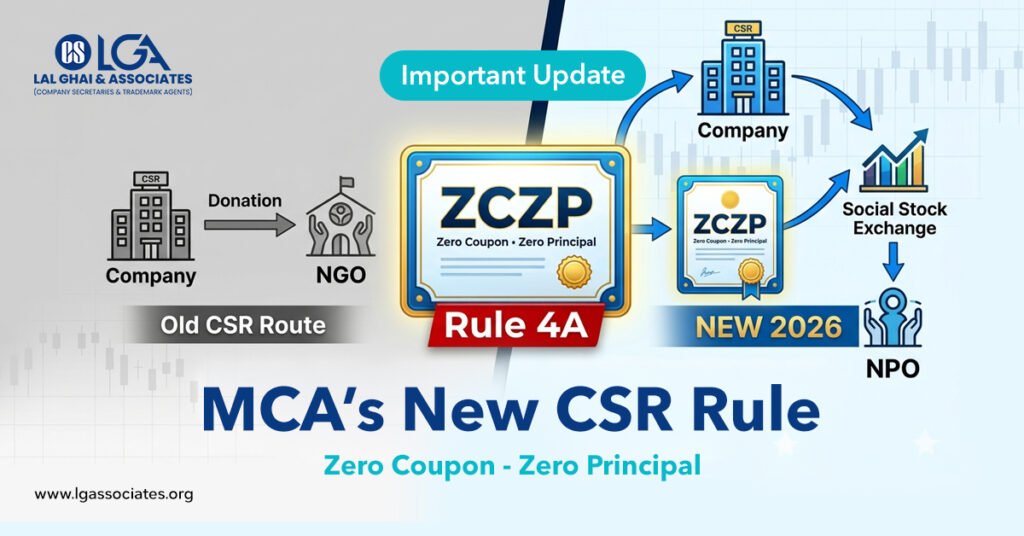

“A company may carry out Corporate Social Responsibility activities through a zero coupon zero principal instrument issued by a Not for Profit Organisation registered with the Social Stock Exchange segment of a recognised Stock Exchange.” — Rule 4A, Companies (CSR Policy) Amendment Rules, 2026

What is a Zero Coupon Zero Principal Instrument?

The amendment inserts a formal definition into Rule 2 of the CSR Rules. A Zero Coupon Zero Principal (ZCZP) Instrument is a financial security with the following characteristics:

- Issued by a Not for Profit Organisation (NPO) registered with the Social Stock Exchange (SSE) segment of a recognised Stock Exchange in India.

- Declared as a security under SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 — specifically as defined under Regulation 292A(e).

- Zero Coupon — meaning it pays no periodic interest or dividend to the investor/subscriber.

- Zero Principal — meaning there is no repayment of invested capital at maturity. The money goes entirely to the social cause.

Key Provisions of the Amendment

Rule 4A(1) CSR Through ZCZP Instrument — Permitted

A company may carry out its CSR activities by subscribing to a zero coupon zero principal instrument issued by an NPO registered with the Social Stock Exchange. This is subject to the condition that the expenditure on such instruments shall NOT exceed 10% of the company’s total CSR expenditure for that financial year.

Rule 4A(2) Impact Assessment Exemption for Subscribers

Companies subscribing to a ZCZP instrument are exempted from conducting an independent impact assessment of any project funded by that instrument. This removes a significant compliance burden from CSR-funding companies, shifting accountability to the NPO and SSE regulatory framework.

Rule 4A(3) Obligations of the Issuing NPO

The NPO issuing the ZCZP instrument must: (a) Undertake a project with a duration of not more than three successive financial years from the date of issue of the instrument; and (b) On termination of listing of such instrument, transfer any unspent amount to a fund included in Schedule VII to the Companies Act, and submit its compliance report to SEBI.

Rule 4A(4) Applicability of Rule 4 Sub-rules

Sub-rules (5) and (6) of Rule 4 of the principal CSR Rules shall also apply to implementation of CSR activities through the ZCZP instrument, ensuring that standard governance safeguards remain in place.

Why This Matters: The Social Stock Exchange Connection

India’s Social Stock Exchange (SSE) was operationalised under SEBI’s framework to bring formal capital market discipline to social sector fundraising. By linking CSR expenditure to SSE-listed NPOs via the ZCZP mechanism, the MCA achieves several policy goals simultaneously:

- Transparency: NPOs must meet SEBI’s listing requirements, including disclosure norms, before they can issue ZCZP instruments.

- Accountability: Unspent funds at the end of a project must be transferred to Schedule VII funds — no diversion is possible.

- Reduced Burden on Companies: Companies are freed from impact assessment obligations for ZCZP-funded projects.

- Mainstream CSR Capital: Corporate India can now route CSR funds into the regulated social capital market rather than managing projects directly.

Practical Implications for Companies

Important Note on the 10% Cap:

The ZCZP route is subject to a ceiling of 10% of the company’s total CSR obligation for a given year. Companies must ensure their overall CSR plan is structured to stay within this limit if using ZCZP instruments.

For companies — particularly listed entities and large private companies — this amendment opens a new, compliant channel to deploy CSR funds efficiently. Instead of setting up implementation agencies or managing projects in-house, they can subscribe to ZCZP instruments issued by SEBI-registered, SSE-listed NPOs.

The amendment is especially relevant for companies that:

- Wish to support social sector organisations working in education, healthcare, rural development, or environment — without the administrative overhead of direct project implementation.

- Are looking for a regulated, auditable channel for CSR spending that satisfies both Board and statutory auditor scrutiny.

- Have historically struggled to utilise CSR budgets fully due to lack of on-ground implementation capacity.

Our View

This is a forward-looking amendment that aligns India’s CSR framework with the broader development of the Social Stock Exchange ecosystem. The SEBI-regulated SSE was always intended to bring market discipline to social funding, and this MCA notification now formally integrates SSE-listed instruments into the corporate compliance toolkit.

Companies should begin reviewing their CSR policies and Board-approved CSR plans to assess whether the ZCZP route is suitable for a portion of their annual CSR obligation. It is equally important to ensure that any NPO they wish to fund is duly registered on the SSE and has issued valid ZCZP instruments under the SEBI framework before any subscription is made and reported in the CSR disclosures.

Given the interplay between MCA’s CSR Rules, SEBI’s ICDR Regulations and the Companies Act’s Schedule VII, professional guidance is strongly recommended before deploying CSR funds through this new mechanism.

Need Guidance on CSR Compliance?

Our team of Company Secretaries at Lal Ghai & Associates can help you structure your CSR policy, identify eligible SSE-listed NPOs, and ensure full regulatory compliance.

www.lgassociates.org | +91-94636 40466 | info@lgassociates.org

This bulletin is prepared for general informational purposes. It does not constitute legal or professional advice. Readers should seek specific advice before acting on any matter covered herein.